Fun isn’t a term associated with late-stage college planning.

Non-Transparent, confusing, and illogical are preferable words involving this ponderous process.

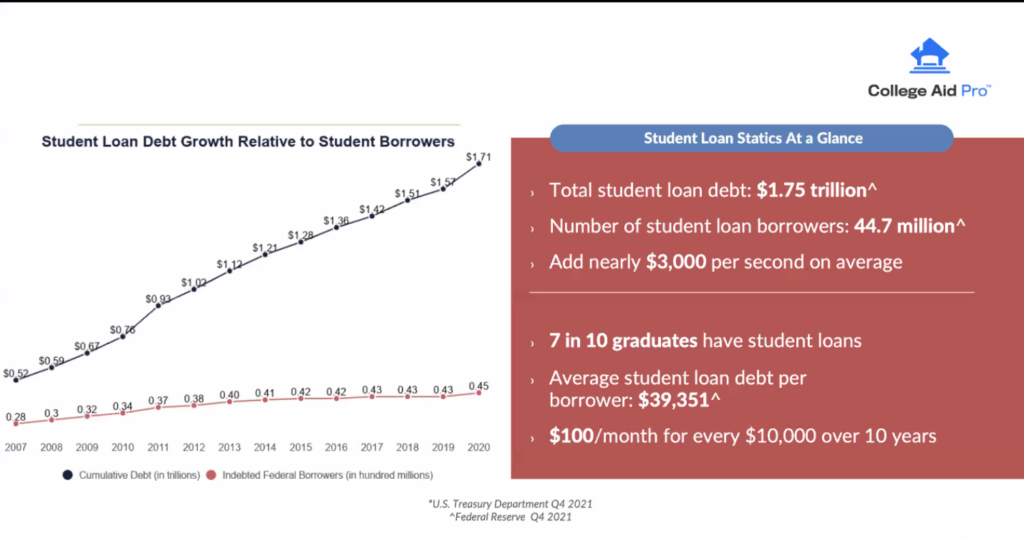

Most financial advisors and high school guidance counselors offer little help deciphering an arcane maze of complexities.

With the opening of both FAFSA and the college application process, it’s time for some clarity to benefit frustrated students and soon-to-be a lot less wealthy parents.

Here’s some information to consider before making a family’s most significant financial commitment besides purchasing a home.

1. FAFSA filings begin October 1. Try to get this completed by the beginning of November. There’s no need to file on the first day; a one-month deadline works for most circumstances.

2. Apply your 2021 taxes for first-year students attending the fall of 2023 semester. The prior-prior year rule becomes the baseline for potential financial aid.

3. If this tax year doesn’t represent typical family income, appeal to the school with a professional judgment to explain the discrepancies.

4. There’s little to lose in filing the FAFSA. A few schools require it for merit aid eligibility. To qualify for the best-structured loans, complete FAFSA. Federal direct loans don’t need a credit check, have no income restrictions, and, most importantly, are in the students rather than the parent’s name.

5. Need-based FAFSA eligibility’s main component is income. Student income reduces aid by 50%, but the first $7,000 is exempt. A high parental income and a large asset base have no effect on Merit Aid which most schools offer.

6. 529 plans are parent assets assessed at a 5.64% needs-based rate. The child is considered the beneficiary; the parent can change beneficiaries at any time.

7. Retirement plan assets don’t count for inclusion in needs-based aid calculations, but contributions are considered untaxed income and added to the parents’ reported income.

8. UTMA accounts are assessed at a 20% rate using FASFA calculations. Rolling this over into a custodial 529 owned by the child lowers the financial aid impact to 5.64%, but potential capital gains may result.

9. The Federal government computes EFC or expected family contribution after submitting the FAFSA. It’s not necessarily an accurate indication of what families can afford but more of a rationing system. Often, the EFC isn’t a realistic assessment of a family’s ability to pay. Be Careful!

10. Family’s EFC is reduced by 50% if a sibling also attends college. This break disappears with the 2024-25 FAFSA.

11. Private scholarships represent a minuscule portion of college funding. Spending time focusing on governmental and school programs is a better use of resources.

12. Community college is much cheaper, but only about 20% of students receive their Bachelor’s degree within six years.

13. High-income parents have an advantage in the admissions process. Due to a conflicted college ranking system, selectivity is at a premium value. Recruiting wealthier students helps colleges move up on the list, increasing their selectivity. Students from affluent families tend to receive higher grades, graduate on time, and find future employment. The system isn’t fair, but these are the game’s rules.

14. Except for the most elite schools, almost everyone receives either merit or needs-based aid. College is a buyers’ market.

15. Athletic scholarships are rare. Only 2% of seniors who competed in high school sports receive NCAA scholarships.

We’ve only touched the surface of this vital but often indecipherable issue. If you have more questions, don’t be afraid to reach out.

In the meantime, I spoke with Ben Carlson recently regarding some of the above and more. You can watch it right here.