Not all insurance involves paying an insurance company.

Instead, paying yourself provides the ultimate coverage.

For most people, their biggest asset is their salary.

Wages fund home purchases, vacations, and your kid’s college tuition. It’s hard planning a retirement without a decent wage.

All things considered equal, a good salary gives you the best chance of achieving your financial goals.

How do we fully insure our most important asset?

Never stop learning.

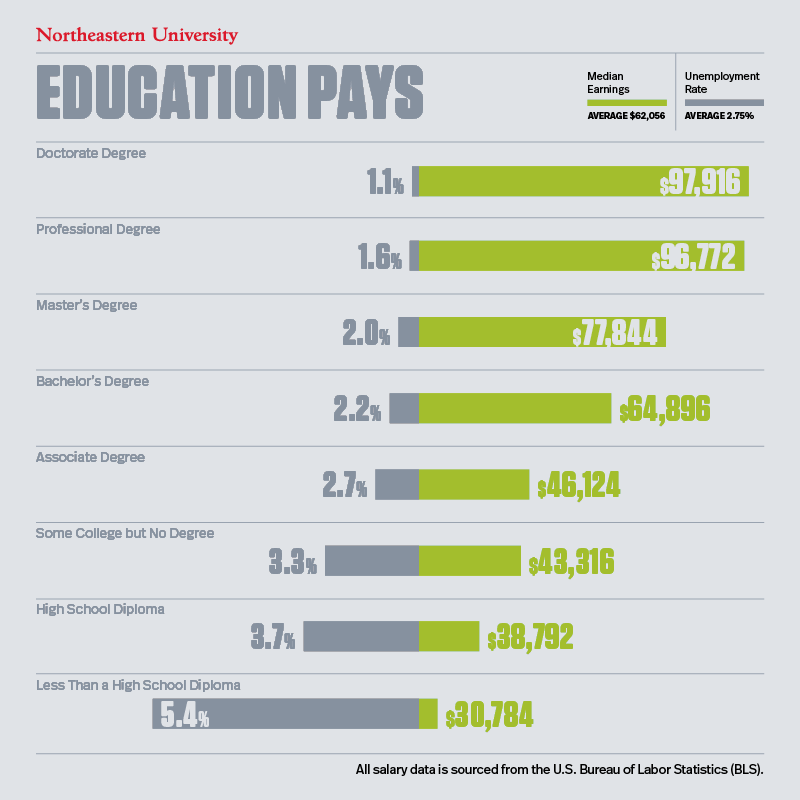

Let’s start with college.

Numbers don’t lie.

According to the Federal Reserve Bank of New York, college graduates with no college degree earn about $78,000 manually. This is $33,000 more than a person with just a High School diploma.

Ron Lieber writes in his terrific book The Price You Pay For College:

The New York Fed estimated the value of that premium over a forty-plus-year career. It concluded that the annual average rate of return on investment in college is about 14%. That figure, which is for people who finish their degrees in four years, is double what most people would be happy to earn in the stock market over time.

This number diminishes to 11% for five-year students and 8% for 6-year graduates. Still not too shabby.

Of course, not all majors produce identical income. over time. Temple University Professor Douglas Webber calculated the gap between the highest and bottom rung majors could add up to $2,000,000 over the course of a working career.

Returns don’t include the Soft Skills the typical college experience generates. As a result, it’s hard to price their value add. These include lifelong friendships, contacts, clubs/activities, and the experience of interacting with students of different cultures.

Weber calculated college graduates are 177 times more likely to earn $4 million and up during their careers than are high school graduates.

What about young people who don’t do well in school and can’t fulfill their potential in a traditional academic setting?

College isn’t for everyone.

Trade School might be a better alternative.

There are many advantages to choosing this route. First, the admissions process is far less complicated. Second, a certification can produce an immediate job opportunity. Trade School is much less expensive than a traditional college with a shorter duration.

College graduates, on average, earn more than their trade school counterparts. That being said, having a vocation doesn’t condemn someone to a life of poverty.

Since schooling is shorter, starting work earlier provides an advantage.

Some schools offer programs with nice income potential.

The College Post points this out.

According to the US Bureau of Labor Statistics, the median pay for construction managers in 2019 was $95,260 per year. Meanwhile, radiation therapists earned $85,560 per year, and dental hygienists cashed in $76,220 annually.

Many of these jobs can’t be outsourced and provide more job security. It’s hard to cut hair, fix your car, plumbing, or electricity through a call center.

Schools are terrific, but they don’t guarantee maximizing learning potential.

There’s only one way to do this. It’s called lifelong learning.

Degrees and certifications are starting blocks. Life-long learning provides the ultimate income protection.

Life is constant change.

Some of the best jobs in the world don’t currently exist.

A life-long learner possesses the ability to seize on these opportunities.

Instead of fixating on knowledge, dance with it.

There’s no peer for life and job satisfaction other than continuous growth and loving the journey.

Unlike snobby Ivy-League schools, this opportunity doesn’t discriminate.

Fools and geniuses provide lessons for us all.

Underinsurance can wreck the most well-thought-out financial plan.

Paying yourself first with lifelong learning is the ultimate insurance product.