Inconvenience isn’t fatal.

Market fears often exceed reality. Replacing facts with noise is an awful way to manage your money.

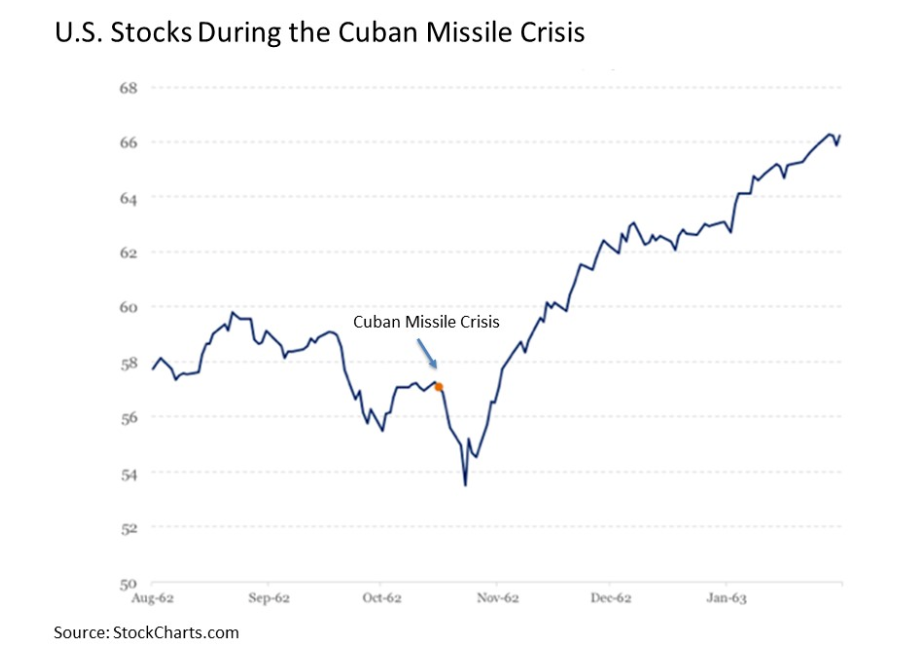

In October of 1962, the world teetered on the brink of catastrophe.

The Cuban Missile Crisis was a defining moment in the realm of absolute risk.

Soviet nuclear missiles turned up in Cuba. The U.S. response was a full-scale naval blockade of the island.

For the next 13 days, an extinction-level event was a realistic possibility.

It almost happened. A Soviet submarine commander nearly launched a nuclear torpedo after being depth-charged.

Communication links between the two superpowers were dangerously archaic. The U.S. had a poor understanding of Russian launch protocols. Contact between leadership groups was slow, incomplete, and error-prone.

World survival hinged on individual restraint, not robust systems.

Though a trivial matter at the time, the financial markets didn’t collapse.

Why?

Markets are not pricing feelings. They are pricing survival and adaptation.

Thank God things ended peacefully, but the Cuban Missile Crisis offers valuable lessons for all investors to heed.

If you cannot emotionally handle non-existential risk, long-term ownership isn’t for you.

Regarding 1961, time erased fear, markets absorbed the shock, and history moved on.

Last week, stock investors sold their positions because they believed the preposterous idea that the U.S. might invade Greenland, resulting in a catastrophic trade war with Europe.

Of course, none of that came true, but the next crisis will undoubtedly result in the same type of panic selling.

Unlike fear during the Cold War. Today’s concerns are simulated, narrated, amplified, and monetized by ever-present algorithims monitoring your emotions 24/7.

In 1961, the world was on the brink of extinction. Today, investors sell because they’re uncomfortable.

We live in a world that has already endured world wars, nuclear brinkmanship, pandemics without vaccines, and depressions without safety nets. Yet investors respond to discomfort as if it were danger.

Markets have experienced the worst humanity has to fear and are still standing.

Those with the intestinal fortitude to see the break in the clouds profit over time with unprecedented wealth.

Emotional fragility resulted in the opposite effect.

Markets couldn’t care less about investors’ feelings. They don’t remember investor sentiment, but they record with precision who stays invested and who does not.

Despite social media’s hyperfocus on all that is wrong with the world, things are dramatically safer and more resilient than ever.

Central bank language, quarterly earnings misses, elecction cycles, and recession fears will always be ever-present.

Today’s AI discussions don’t involve nuclear payloads.

An investor’s main priority is gaining the proper perspective.

What matters is understanding the difference between inconveniences and fatalities.

Today’s fears very often exceed reality, turning them into noise.

Remember this next week when talk of a Canadian invasion or whatever else imaginary crisis du jour emerges.

Even though 1961 exists now in a few pages of history textbooks, the threat was real.

There was a bull market in fallout shelter construction, schools ran terrifying nuclear drills, and Americans crowded into midnight mass as if their lives depended on it.

Ponder this the next time you watch a Prophet of Doom video on TikTok.

There’s a vast chasm between ordinary discomfort and real danger.