All or nothing is a dangerous strategy regarding Warfare and Investing.

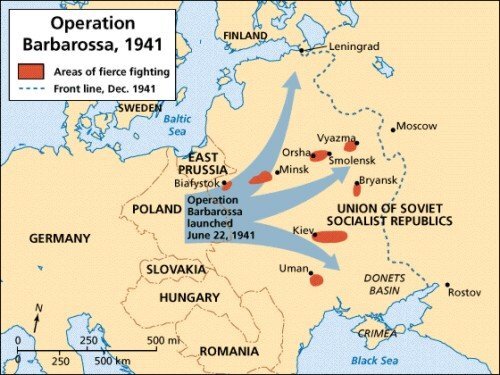

In all modern warfare, there’s never been more devastating carnage than when Nazi Germany invaded the U.S.S.R. in 1941.

Operation Barbarossa led to the highest recorded amount of war dead in the history of humanity.

Germany mobilized 17,500,000 soldiers to partake in the invasion. 5,365,000 ended up dead or missing.

Russia sent 34,000,000 men and women to defend the Motherland. 8,640,000 never returned home.

These figures didn’t include at least 13,000,000 soviet civilians who died during the German invasion. Many perished from starvation, executions, and scorched-earth policies.

Soviet Soldiers feared their government, led by tyrannical dictator Josef Stalin, more than the encroaching Nazis.

On July 28, 1942, during the darkest days of the war, Stalin issued his infamous Order No. 227, also known as “Not One Step Back.”

The order forbade unauthorized withdrawals, and officers were bound to “fight to the last man.”

Commanders who disobeyed the edict were court-martialled and usually executed. The order included other “incentives’ like placing barrier troops behind the frontline soldiers whose job it was to shoot any soldiers attempting to flee without permission.

Soldiers thought to be cowards found themselves shipped to suicidal penal units used for tasks like clearing mine fields without the luxury of mine detectors.

Stalin supposedly remarked, “It takes a brave man to be a coward in the Red Army.”

Luckily for investors, they don’t have to choose between kill or be killed on a frozen Russian battlefield.

Unlike this ultimate example of a Zero-sum game, investors have choices and can make balanced decisions regarding managing their finances.

Since there isn’t an insane Dictator issuing Order No. 227, you have the opportunity to compromise, unlike the poor Russian souls ordered to become human mine-sweepers.

Here are five personal finance tradeoffs that don’t involve Total War strategies:

- Paying Off Debt vs. Investing: It is ideal to start paying off your highest-interest-rate debt while still investing enough to qualify for your employer’s 401 (k) match. You will accomplish two vital goals that will bode well for your future self if possible.

- Spending vs. Saving: Establishing a reverse budget in which you save first and then spend the rest will help you make more guilt-free decisions and bring automation rather than micromanagement to your budget.

- Renting vs. Buying a Home: There’s another option: rent while saving for your home purchase, or buy a more modest home and accomplish your goal without breaking your budget.

- Helping Adult Children vs. Securing Retirement: A critical word in the dictionary to aid you in this decision is boundaries. You can offer your kids limited help without jeopardizing your financial security. One-time items rather than steady contributions will keep the cupboard from becoming bare when you most need the funds.

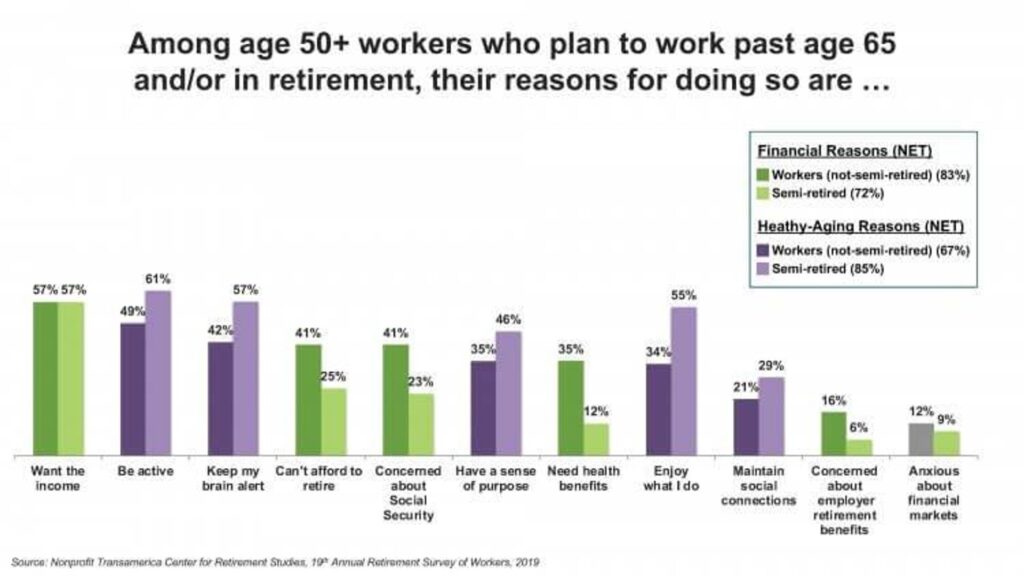

- Working Full-Time vs. Retiring Completely: There’s no iron rule that you must implement a hard stop to your career. Opportunities abound in consulting or working part-time to ease your way into the second part of life with the bonus of extra income and more compounding of your retirement assets.

Financial freedom means you can take a step back to make the best use of the plethora of choices in a well-designed retirement plan.

Fortunately, none involve fighting at the Russian Front with the enemy in front and behind you.