Are we going backward, or are we going forward?

In the” Good Old Days,” Robber Barrons devised a scheme for creating corporate feudal systems, making employees virtual indentured servants. Company scrip became a substitute for government-issued currency. Scrip was prevalent in numerous mining and logging camps before being outlawed in 1938 as part of the Fair Labor Standards Act.

In these remote locations, workers received their pay in scrip. Since there was no competition, employees purchased essentials at the company store. These stores were monopolies and placed huge mark-ups on their products.

Exorbitant fees prevented workers from exchanging scrip for hard currency. The company store system made workers dependent on their employers, making it almost impossible to sever a forced loyalty.

While nothing like the bygone days of company towns, young people today are encouraged to take on more debt than they can handle. Without intervention, the cycle could spiral into a life of working to pay others instead of oneself.

Recently, I was helping a young person with their student loans. After viewing their loan portfolio, one contract stood out. It was a private student loan from a bank, and the annual rate was almost 19%! Companies need to generate profits and manage their risk. We all get that, but there are limits on everything.

We can all agree that lending money at such high rates to 20-year-olds with little or no financial literacy doesn’t benefit our nation’s future in any way. Mandatory Counseling should alert young borrowers to the hazards of such a deal before they sign anything.

After- all, we put warning labels on cigarettes, don’t we?

One can argue that education has an ROI based on lifetime salary potential with reasonable costs. The same doesn’t apply to the following scheme designed to snare gullible youngsters in debt servitude.

Reverse compounding should be at the center of your financial plan – said no one ever.

Last week, DoorDash announced a partnership with AI-powered payment network Klarna, enabling DoorDash customers to order food and pay on an installment plan.

What could possibly go wrong here?

There are many skeptics regarding this arrangement. Many of the comments on social media went something like this:

“If you’re financing your DoorDash deliveries, you aren’t living paycheck to paycheck, you’re just a moron.”

Klarna and DoorDash defended their position by mentioning that Kalrna offers an interest-free Pay in Full or Pay in 4 option. The company also noted that, unlike a credit card, services are restricted if a customer misses a payment.

Others weren’t impressed. Kevin Thompson, a fiance expert, told Newsweek;

This shouldn’t be allowed. Nothing good comes from it—just more debt. We’re walking into a modern-day version of feudalism, where people want to eat but are kept in line by digital debt overlords.”

Alex Beene, a financial literacy instructor for the University of Tennessee, added:

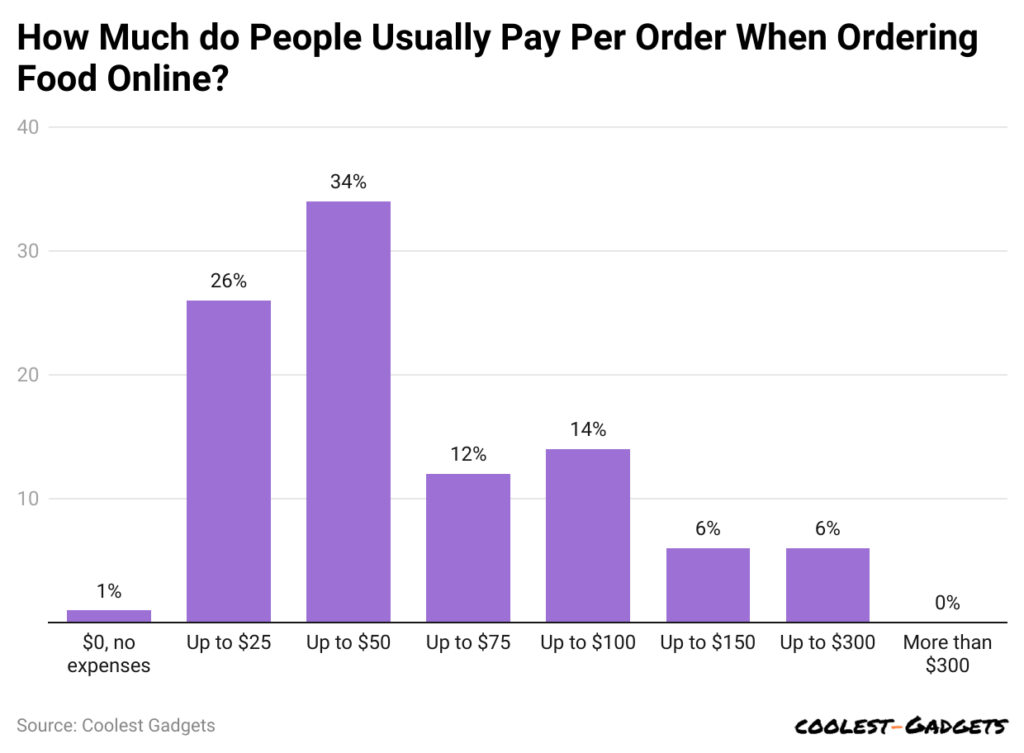

“Past reports have estimated the average DoorDash order to be between 30-to-40 dollars, though. When you see financing being pushed for smaller purchases, it raises a financial red flag that customers who are already tapped out are being encouraged to use debt products for buying items they shouldn’t have to seek financing for every day.”

Students don’t need to take out pricey loans to get an excellent college education.

The same rationale applies to buying a Bacon-Double Cheese Burger.

It’s hard enough being a young adult without a hefty debt burden.

It’s time for creditors to pick on someone their own size.