Managing Risk is more than your portfolio percentage of stocks to bonds.

No asset allocation negates the ravages of chronic disease, not to mention an early demise.

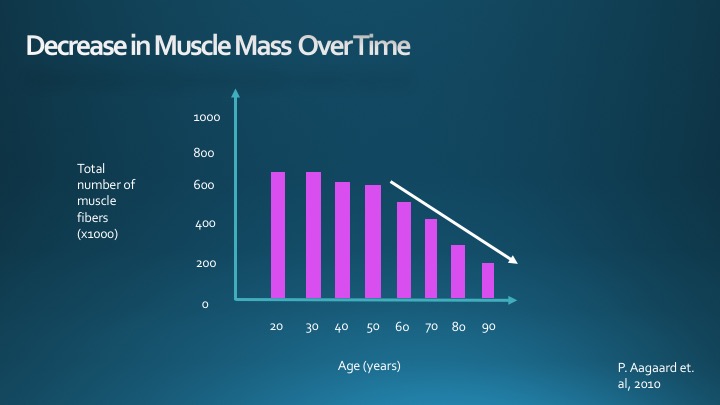

Keeping yourself in shape must be a priority in any goals-based financial plan. Nothing comes in a close second.

Even power brokers on Wall Street are taking this message to heart.

Bloomberg recently spotlighted this trend. Columnist Chris Bryant remarked: Deadlifts beat discounted cash flow on the new buff Wall Street.

Devotees include Goldman Boss David Solomon and Morgan Stanley Executive Chairman James Gorman.

Bryant writes: People who spend their working lives trying to manage Risk in return for long-term financial gain often fail to apply those lessons to their health. That’s partly because balancing personal well-being and professional success can be difficult in an industry that valorizes long hours and now wants workers back in the office. But while finance hasn’t become a walk in the park, there is more awareness of the need to keep physically healthy and mentally resilient.

Finally, the so-called Masters of the Universe got a market call correct, and they didn’t even have to resort to decimal points.

What about the rest of us?

Is health the ultimate form of wealth?

How do I get started?

The good news is that one doesn’t have to attend a fancy gym to get equal or better results. There’s a cult New York Gym called The Dogpound. Annual memberships can run up to $36,000 yearly. (Not a typo.)

Let’s examine how the average retiree can improve their quality of life without relying on a bull market to finance their dreams or flexing with Gym Bros.

Starting saving for retirement at age 70 is a bad idea. Starting an exercise program at 72 is just the opposite.

Take a look at Richard Morgan. He’s a 93-year-old, four-time rowing champion with the fitness levels of a 40-year-old.

This is Richard Morgan.

He's a 93-year-old four time world rowing champion who has the fitness levels of a 40 year old.

Scientists studied him to find out his secrets to delaying the aging process.

Here's what they found: pic.twitter.com/RGhP9LQg9A

— Dan Go (@FitFounder) April 13, 2024

What can we learn from Mr. Morgan? According to Dan Go – plenty.

- It’s never too late to start. Richard started rowing at age 72. Before this undertaking, he lived a sedentary lifestyle. Not bad for someone who has won four world titles in rowing for his age group.

- Limit your body fat. According to a bioimpedance scan, Morgan’s level is 15.4%. Many people half his Age carry double this percentage.

- Chronological Age is a distraction. Based on several metrics, Richard is fitter than the average 40-year-old.

- Consistency is more important than perfection in a training program. Morgan rows 20 miles weekly at various intensities and completes 2-3 resistance training workouts. Showing up is 90% of the battle.

- You can’t out-exercise a poor diet. Morgan avoids most processed foods and consumes .8 grams of protein per body weight daily.

If you’re already adept at saving for retirement, getting yourself into shape isn’t out of your comfort zone, despite what you may think.

Accumulating wealth and maintaining optimum health are guided by a similar North Star: consistency, not perfection.

Start by transferring the discipline of your saving habits into a workout program you can stick with. You’ve already proven that compounding and long-term planning are a part of your DNA. Apply these same habits used to grow your nest egg into reshaping your body.

Dollar-cost average your energy into healthful activities, and the returns might surprise you.

The stock market isn’t the only thing that benefits from compounding.

If you’re still a skeptic, ask 40-year-old – I mean 93-year-old Richard Morgan.