Evolve or suffer slowly.

Retirement planning is afflicted by many maladies found in modern medicine. Lifestyle management trumps portfolio management. Treating financial symptoms and not the disease sabotages our financial plans and health.

Peter Attia points out the differences in the evolution of medical care.

Medicine 1.0 refers to medicine based on intuition and trial and error, not science. The idea of doing no harm was the founding principle. Unfortunately, the lack of evidence-based treatments killed more patients than the diseases themselves.

Medicine 2.0 emerged in the 20th century. It’s characterized by standardization, efficiency, and specialization. While a massive improvement over Medicine 2.0., it’s not the ideal solution. Treatments are often based on statistical models rather than individual patient characteristics. Early intervention focusing on nutrition, exercise, and sleep aren’t part of the protocol. By the time patients receive treatment. It’s often too late.

Medicine 3.0 is the holy grail of healthcare. Personalized medicine tailored to the individual needs of patients is the ideal remedy. The emphasis falls upon prevention and lifestyle interventions before disease enters the body. Patients are empowered to take an active role in their health care. Medicine 3.0 is the answer to the chronic disease epidemic afflicting our nation.

Dr. Attia sums things up. The goal of this new medicine-which I call Medicine 3.0-is not to patch people up and get them out the door, removing their tumors and hoping for the best, but rather to prevent the tumors from appearing and spreading in the first place or to avoid the heart attack. Or to divert someone from the path to Alzheimer’s disease. Our treatments and prevention and detection strategies need to change to fit the nature of these diseases, with their long slow prologues.

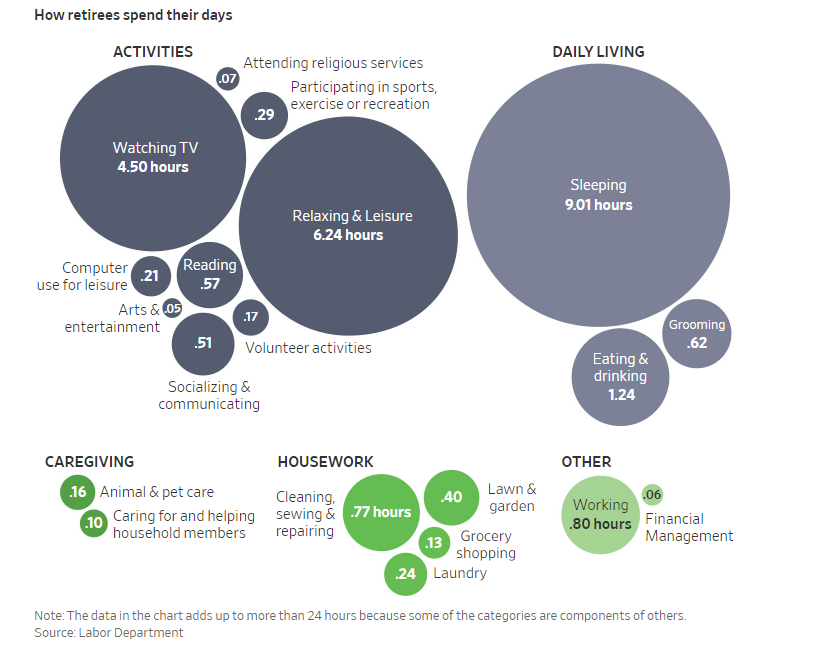

Retirement planning suffers from many of the same misconceptions as Medicine 2.0. Retirees are put into a neat box sealed with a number attached to the retirement date. The cookie-cutter approach is scalable and standardized. It’s perfect for a robot, not a human being.

What about the long slow prologue?

What good is money if you can’t move or die early?

How can we individualize the process and empower retirees?

Retirement can be a form of chronic disease. Isolation, depression, and feelings of worthlessness can be the side effects of early retirement and portfolio optimization.

Planning what to do with one’s time is more critical than accumulating money.

Retirement plans must start focusing on healthspan rather than lifespan.

Living and being alive are two different things. A Monte Carlo simulation or sequence risk doesn’t factor in the most crucial return – the quality of life.

Retirement planning without focusing on nutrition, sleep, exercise, and mental health falls short of the main goal, despite what a spreadsheet might say.

The best risk management strategy is taking care of your mind and body, not regular rebalancing.

Financial planners, personal trainers, nutritionists, second career counselors, and therapists are vital Retirement 3.0 team members.

Retirement 3.0 is about empowerment and prevention.

Dr. Attia speaks about training NOW for the Centenarian Decathlon. This includes doing things like these at the advanced age of 100.

Hiking 1.5 miles on a hilly trail.

Picking up a young child from the floor.

Carrying two five-pound bags of groceries for five blocks.

Lifting a twenty-pound suitcase into the overhead compartment of a plane.

Doing thirty consecutive jump-rope skips.

Evolve into a retirement 3.0 mindset.

Your retirement need not become another chronic disease.