Warning labels should be attached to travel teams and high fee investments.

Both are dangerous to your health and wealth.

TD Ameritrade estimates that 63% of American families spend between $100 and $500 per child a month on youth sports.

Astonishingly, 20% spend more than $12,000 a year.

Sports are terrific.They teach many essential life lessons like leadership, discipline and teamwork. My sons play several sports and my cousin Frank is a big-time sportswriter. I love watching and going to different events-even professional wrestling.

Why?-because it’s fun.

This isn’t the motivation for delusional parents who take games way too seriously.

According to TD, 66% spend money because they think their “investment” will lead to an athletic scholarship.

Worse, some believe a pro career is in the cards.

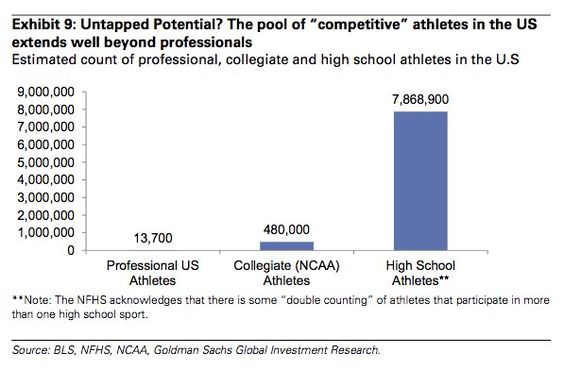

Good luck! Do you think a 6% chance of making a college team, 2% to make a top college team, and a less than 1% for turning pro are good odds?

Investors have unreasonable return expectations for high-cost investments. They pay up for the privelege.

Simple and inexpensive index funds trounce most stock pickers over long periods. Unlike the chances of your kid playing Division I sports, the odds are in your favor.

Lower returns produce a reverse compounding effect. Working longer, and a lower standard of living in retirement are the consequences.

You get what you don’t pay for when you invest.

The same rules apply to travel teams.

Parents invest hoping for a winning lottery ticket. Not smart when saving for retirement or investing in your child’s future.

Like concentrated high-cost stock investments, a heavy portfolio allocation to expensive travel teams is saturated with unintended negative consequences.

A survey by i9 Sports, a youth sports league franchise, uncovered nasty things lurking around the dark underbelly of this $15 Billion industry.

65% of moms say their kid’s sports schedules interfere with their jobs. 24% resent these commitments. Great stress is put on the children. As parents increase their investments, they demand higher returns.

No different from investors who overpay high priced portfolio managers to “beat” the market. This usually ends in tears. Sadly, the tears of your children leave longer lasting scars than losing a few dollars in the market.

Never mind the physical pain from injury due to gruelling schedules and specializing in one sport at an early age.

As pressure mounts, some parents become verbally and physically abusive to kids, officials, and coaches. A few sue coaches for benching their children for depriving their kid an opportunity to win a scholarship.

Like the tech bubble, parent expectations become “irrationally exuberant.”

The more time and money they spend, the worse this gets.

Parents ignore the high probability bet. How about opening a 529 college savings plan ?

$500 per month, 7% annual return over 18 years = $203,994. Not sexy like the “cool kids” travel team but a pretty good R.O.I.

Did the private “speed” coach provide this return?

Proper investing lets us go back to having fun at games instead of turning them into death matches.

Parents travel hundreds of miles chasing fool’s gold on the travel team’s playing fields. 68% of people never heard of a 529.

“It’s definitely taken over everything,” says Magali Sanchez, a legal records clerk from San Diego whose daughter Melanie Barcenas, 9, and son Xzavier Barcenas, 8, play travel soccer. To help pay for their fees, Sanchez’s husband Carlos, a gas-station attendant, will spend 12 hours on Saturday carting supplies at tournaments. Practice and tournaments overtake nights and weekends like kudzu–Sanchez says they often have to skip family weddings and kids’ birthday parties. “This sports lifestyle is crazy,” she says. “But they’re your kids. You do anything for them.” Time Magazine

Sometimes this means doing less.

Sources, Pricing Kids Off The Playing Field, by Robert Carle, Newsday, How Sports Became A $15 Billion Industry, by Sean Gregory, Time Magazine