Why would anyone pay $5,000 for a $50,000 death benefit?

Planning for your own demise can be very expensive; in more ways than one.

Some insurance companies unearth many ways to profit from your worst fears. The credo: “If they cry they buy” sells a lot of products people don’t need.

Case in point: the variable annuity. Most investors do not need this product, and certainly not the high-fee variety that they are frequently sold.

The “Mortality and Expense Fee” or Guaranteed Minimum Death Benefit is a waste of money for most. This benefit “guarantees” to pay the higher of your combined premiums or the cash value of your annuity at the time of your death.

For purposes of brevity, let’s leave out the sub-account fees, income riders, administrative fees and (possible) wrap account charges that are typically part of the annuity fee-orgy. This one is bad enough by itself.

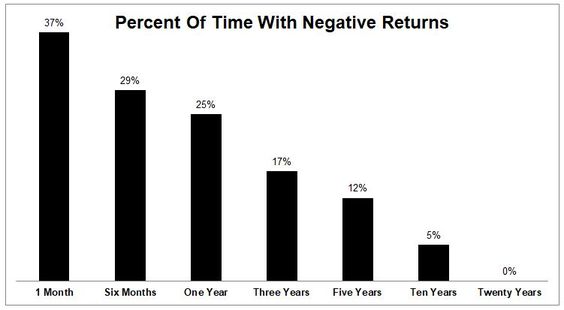

Young investors have a time horizon measured in decades. The chance they will collect this insurance is basically zero. Markets over this span have never had a cumulative negative return.

Source: Michael Batnick

Why do so many millennial teachers we encounter own these products? Could it be a portion of this Mortality and Expense fee goes toward commissions?

We don’t need Sherlock Holmes to decipher this clue.

Mortality and expense premiums are not like what you pay for home, auto, or disability policies. There is little chance long-term investors will collect a penny. This expense “insures” your investment will dramatically underperform the market.

What about a person with a shorter time horizon? It turns out this deal might be even worse!

James Osborne points this out in his article, “Insurance Premiums For A Nonexistent Death Benefit”. Many older investors are paying more and receiving less in their variable annuities because of the nine-year bull market.

He gives an example of someone who invested $200,000 in a variable annuity in 2007; it now has a value of $300,000.

“So now Joan is paying her 1.75% internal fee to protect a GMDB that is 33% less than the current cash value of her contract. And – get this – she isn’t paying 1.75% of $200,000 ($3,500/yr.). She is paying 1.75% of $300,000 ($5,250).”

“Higher insurance costs for an insurance benefit that becomes less and less likely to pay out any value over time. Even if her contract value fell by 50% and a piano fell on her, Joan’s heirs would receive an insurance benefit of $50,000 ($300,000 / 2 =$150,000. $200,000 GMDB – $150,000 Cash Value = $50,000 Actual Insurance Benefit). So this year she pays over $5,000 for a death benefit that might be worth $50,000. That is some insanely expensive life insurance.”

Possible strategies to consider:

- For those who own this product in a retirement account: This mess can be undone; first, stop all contributions. Luckily selling an annuity in a retirement account is not a taxable event; however, there is the matter of surrender fees that handcuff investors. Owning this product for 10 years or more should result in minimal surrender charges, though we have seen products with rolling charges and 15-year holding requirements! For those who haven’t owned the annuity for a long time, the solution is something insurance companies won’t ever advertise. Policyholders are allowed to move 10% of the account value, annually, without ANY surrender charges. It might make sense to bite the bullet and start fresh, though, because paying the surrender charge and moving on could save a ton of money over time. Look at these fees and create a strategy to transfer money to a more appropriate investment (like a low-cost index fund).

- Longer-term variable annuity owners in a taxable account can transfer to a no-load, inexpensive annuity product. The only way to avoid the taxes associated with getting out of the contract is a tax-free 1035 exchange. Selling the annuity outright might create an unfavorable tax event. There are low-cost annuities out there that can easily take the place of a higher cost product and not trigger a taxable event, provided a 1035 exchange is used.

In the words of James Osborne, “You can skip the whole GMDB charade.”

If you are a teacher or someone else who owns a variable annuity, we can take a look and give you an honest, non-conflicted opinion on what steps to take.

Preparing for your death is bad enough, paying unnecessary insurance premiums while you are living makes it even worse.

Source: “Insurance Premiums For A Nonexistent Death Benefit” by James Osborne