Conflicted corporate cultures are duplicitously devising ways to contaminate low-cost index funds. Theses toxic germs poison everything in their path. The blight of high fees shows no mercy. This mutating virus infiltrates even the most formidable financial immune systems.

Daren Fonda defended the faith in his outstanding Barron’s article, Investors Might Be Paying Too Much for These Index Funds (from which I am quoting in this post). He exposes market-tracking index funds, from the likes of J.P. Morgan and Wells Fargo, which charge over 1%. Better-informed investors can currently purchase identical funds from Vanguard and others at a 90% discount.

Fidelity offers some index funds for free. (Beware. There’s a big difference between cheap and free.)

But the winner of the “I Wouldn’t Sell This Crap to My Worst Enemy Award” goes to Guggenheim Partners. The C-class shares of Rydex S&P 500 (RYSYX) charges an unfathomable 2.33%!

Leveraged funds and high-cost annuities are also components of their anti-social product lineup.

Product pushers are jumping on the indexing bandwagon. They made a winning bet that many consumers don’t understand the biggest benefit of these products – low costs.

“Decades later, with so many inexpensive mutual funds and exchange-traded funds now available, there’s no reason for investors to pay more than a few hundredths of a percentage point in expenses,” says Tony Isola, an adviser with Ritholtz Wealth Management. “These high-fee funds are taking advantage of the indexing trend but defeating the purpose behind it.”

Not surprisingly, RYSYX vastly underperformed the S&P 500 since May 31, 2006. According to Fonda: Rydex has sold this fund since May 31, 2006. It has returned an average 4.9% since then, trailing the S&P 500’s 7.4% return, according to FactSet. Over that period, the Rydex fund returned 83.1% cumulatively versus 145% for the S&P 500.

Guggenheim didn’t respond to Barron’s requests for comment.

It’s hard to defend the indefensible.

We see this on a daily basis. Teachers are victims of a classic financial bait and switch. It’s partially correct; they own index funds in their 403(b) accounts.

There’s a catch. These investments are held in variable annuity sub-accounts, swarming with layers of insurance, commission, management, and administrative fees.

According to Morningstar, $106 billion in assets are held in index fund sub-accounts averaging 0.59% in expenses.

A 1% index fund is appalling; the costs of these annuities are highway robbery, as the Barron’s article exposes:

“Funds in annuities can be packed with “trailing commissions,” fees that compensate brokers for selling products, says Jeffrey Cutter, a financial advisor in Falmouth, Mass. “People’s chins are on the floor,” he says, when they find out the total costs in annuities, which can add up to nearly 6% in administrative and fund expenses.

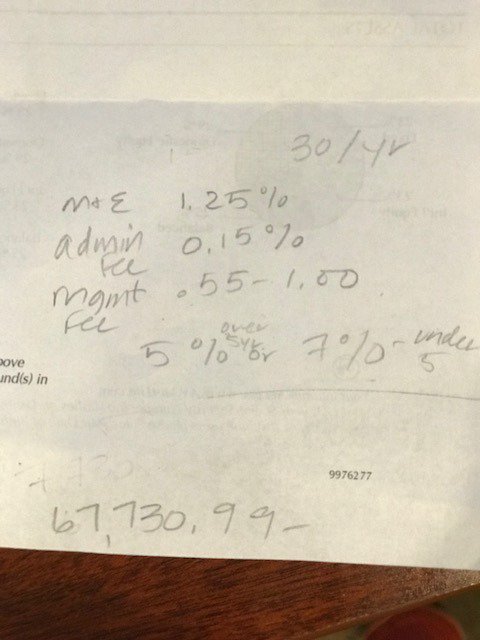

(Here are some of our notes on a 7% fee retirement annuity held by a client.)

Complex and voluminous prospectuses do not disclose costs transparently. Seasoned advisors can’t decipher hundreds of pages of legalese.

Why are unmanaged index funds shamelessly priced?

Three reasons:

- Salespeople don’t work for free.

- Upper management needs to collect exorbitant bonuses.

- Creating shareholder value reigns supreme over the interests of stakeholders.

Sunlight is the best disinfectant to out this financial V.D. Unfortunately, only a supernova will eradicate this deeply ingrained, exploitative culture.

Make a New Year’s resolution to eradicate these retirement cancers from your portfolio.

The good news – unlike a terminal illness – there is a cure.