Unlike the evasive WMD’s that were never found in the Iraqi desert, expensive and inappropriate annuities are all the rage in many teachers retirement plans. This practice must be stopped before the retirement dreams of many educators are blown to smithereens.

William Bernstein, one of the sharpest minds in the investment world once stated, “The typical 403(b) plan contains some of the most egregiously expensive choices in the the entire universe of investing.”

The main culprit for this would be the variable annuity. For a little background history, teachers’ retirement plans were first created in 1958. Originally, they only allowed annuities as investments and were referred to as TDAs, or Tax Deferred Annuities.

In 1974 the 403(b) plan was originated, which also allowed mutual funds to be included in the plan’s choices. Unfortunately, many unscrupulous insurance salespeople still refer to the 403(b) as a T.D.A or T.S.A (Tax Sheltered Annuity.) This misleads many teachers into thinking their only choice for their plans are these ill-suited investments.

This is one of the many little known dirty tricks in the murky underworld of the 403(b). The reason for this deception can be defined in one word: fees. Annuities often cost 2-3% for their annual expenses, plus a 5% payout to the salesperson. The heavy surrender fees enable the insurance companies to fund these exorbitant commissions.

They act as a form of blackmail to the purchaser and guarantee that the insurance company will get their commission money back even if the teacher decides to get out of this inappropriate product within the first ten years or so of purchasing it.

To add insult to injury, many of these surrender charges are “rolling,” which means they reset every time a new purchase is made. This virtually guarantees paying a surrender charge in perpetuity.

Besides earning high commissions, salespeople can also receive meals, vacations, watches and even sports memorabilia for peddling these dogs. This little known fact was disclosed by Senator Elizabeth Warren in a recent report regarding 15 of the nation’s largest insurance companies.

The reason for such high annual expenses is the insurance component built into the product. I like to call this “meteor insurance”. We could all purchase meteor insurance and cover ourselves for an event that is unlikely to happen. But, even if the unthinkable occurred, who would be left to collect from?

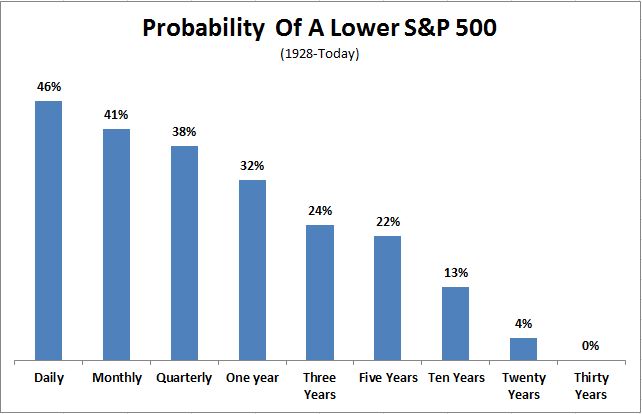

An owner of a variable annuity with an insurance component is guaranteed to get the original investment back at retirement. While this sounds all well and good, for a long-term investor the proposition is rather silly. An investor has never lost money over any twenty-year period in the broad U.S. stock market. The concept that costly insurance is needed for an investor in the broad market with a several decade time horizon is highly questionable.

Insurance is also pitched as protection in the case of premature death. While it would be nice to the principal back at death for the protection of loved ones, this objective can be accomplished much more cheaply and efficiently with a low-cost term life policy. An agent probably will not mention because term insurance does not offer an upfront 5% commission or tickets to a concert!

Why annuities are even permitted in tax-deferred accounts, such as 403(b) plans or IRAs, is questionable. Teachers already receive this benefit in the 403(b) structure. They could own low- cost mutual funds and get the same tax shelter without paying through the teeth!. I liken this to wearing both a belt and suspenders.

Low-cost annuities do have some value for a select few. Anyone who has maximized their retirement plan contributions (such as 403(b) for 401(k) and who have also maxed out their IRA accounts might benefit from owning a low-cost annuity (emphasis on low cost).

There is absolutely no evidence-based justification for over 70% of the assets in 403(b) plans to be comprised of various types of annuities! These complicated and inappropriate products are a major reason why teacher participation rates in their retirement plans languishes at a dreadful 30%!

Most teachers are contributing nowhere near these levels. Purchasing an annuity in a tax- deferred account is akin to a young family buying a luxurious retirement condo before purchasing their starter home.

I would be surprised to find a 401(k) plan with these products as the rule, rather than the exception. Why is it that teachers, one our society’s most valuable assets, are treated in this manner? The answer lies in the amazing fact that their employers are not obligated to look out for their best interests as fiduciaries (unlike in 401(k) plans).

This allows insurance companies using salespeople, masquerading as advisors, to breed these products and multiply them like rabbits across the teacher landscape. We will leave this story for another day.

To sum things up, he idea of putting variable annuities inside 403(b) plans confirms one of the oldest lines about Wall Street: The game has always been to get as rich as possible without going to jail.

{kind=link}